Table of Content

If you're ready to lock in a low fixed rate home loan, chat to one of our friendly lending specialists today. The interest rate is important because it plays a huge role in determining the size of your regular repayments and the total mortgage amount you will repay over the life of the loan. A fixed-rate home loan simply means that the interest rate remains the same throughout the fixed rate term of the loan.

Treasury bond yields, rising inflation and the Federal Reserve’s monetary policy indirectly influence mortgage rates. As inflation increases, the Fed reacts by applying more aggressive monetary policy, which invariably leads to higher mortgage rates. While the interest rate remains the same throughout the loan tenure in a fixed interest rate, the applicant can easily repay the loan. However, in case of floating interest rate you can take advantage of the lower interest rates during the loan tenure. Yes, if another bank is offering you a lower rate of interest on your existing home loan, then you can opt for a home loan balance transfer. However, it is important to check with your bank whether it offers a home loan balance transfer facility or not.

Non-Amortized Loans

This charge is what refer to as interest, and it can be either fixed or variable. Alternatively, if the primary objective of a borrower is to mitigate risk, a fixed rate is better. Although the debt may be more expensive, the borrower will know exactly what their assessments and paydown schedule will look like and cost. A fixed interest rate loan is a loan where the interest rate on the loan remains the same for the life of the loan.

At the current average rate, you'll pay $627.47 per month in principal and interest for every $100,000 you borrow. The average 30-year fixed-refinance rate is 6.43 percent, down 25 basis points from a week ago. A month ago, the average rate on a 30-year fixed refinance was higher, at 6.90 percent. At the current average rate, you'll pay $635.36 per month in principal and interest for every $100,000 you borrow. Just because you might be able to afford more house with a 30-year loan doesn’t mean you should stretch your budget to the breaking point. Give yourself some breathing room for other financial goals and unexpected expenses.

The Bankrate promise

For example, a 30-year fixed-rate mortgage keeps the same interest rate for the whole 30-year period. Your monthly loan payment calculation is based on the interest rate, so locking in the rate results in the same principal and interest payment every month. While this does present opportunities for lower interest rates, you may also be assessed interest at higher rates that are increasingly growing. There is no way of knowing what your future interest rate assessments will be under a variable rate contract.

If you're an existing customer and want to check your current interest rate please login to the ING app, select your home loan and the Interest Rate tab to view your home loan interest rate. Specific mortgage interest rates will vary based on factors including credit score, down payment, debt-to-income ratio and loan-to-value ratio. Generally, you want a good credit score, a higher down payment, a lower DTI and a lower LTV to get a lower interest rate.

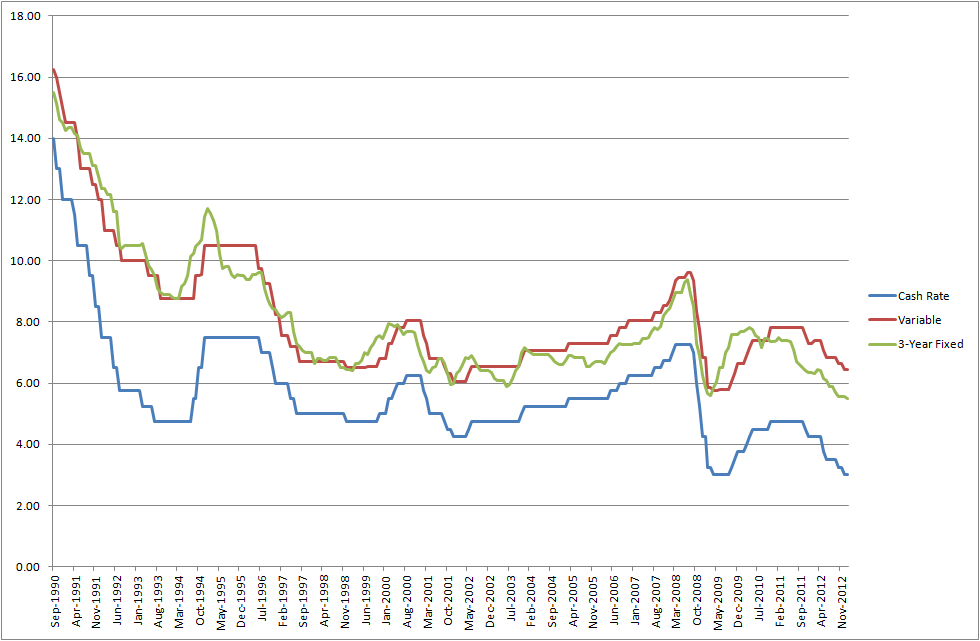

Compare some of Australia's best fixed-rate home loans for December 2022

Fixed-rate loans typically have an interest rate that’s slightly higher than a variable-rate loan’s initial rate. A fixed rate can eliminate the risk of payment shock due to rising rates. Because the rate is fixed, your monthly payment should not change.

This is for your benefit and the lender's, as you wouldn’t want to lock yourself into a record-high rate and then miss out on lower rates in the future. On the other hand, lenders earn profits from the interest you pay, so it’s not in their best interest to let homeowners stay on record-low rates for 20+ years either. Mortgage points represent a percentage of an underlying loan amount—one point equals 1% of the loan amount.

These loans typically charge monthly interest based on a fixed rate. Borrowers make monthly payments of interest, with no payment of principal required until a specified date. Every fixed-rate mortgage has a set interest rate, a set payment schedule and a set term. For instance, a home loan might be at 3.75% for 30 years with monthly payments. A commercial property loan might be at 5% for 15 years with quarterly payments. In any event, with a fixed-rate loan, the borrower will know exactly what their payment is for the entire term of the loan.

If, for example, a lender offers a fixed rate of, say, 6%, its variable rate will usually begin several percentage points lower. While initial interest rates on an ARM may be low, once they begin to adjust, the rates will typically be higher than those on a fixed-rate loan. During the subprime mortgage crisis, many borrowers found that their monthly mortgage payments had become unmanageable once their rates started to adjust. A 30-year, fixed-rate mortgage is the most popular home purchase financial product because it’s often more affordable than other shorter-term mortgage loans. That gives homeowners a little more wiggle room in their budget, while keeping the certainty that the monthly payment will never change.

Fixed rates do not fall during periods of declining interest rates. Fixed rates do not rise during periods of rising interest rates. The interest rate for a variable loan is generally lower than a fixed loan, especially when the loan is incurred. Loans typically get better upfront perks like low introductory rates for an initial loan period.

The most popular ARM is called the 5/1 ARM, which has a fixed rate for the first five years of the loan and then switches to an adjustable rate for the remainder of the 30-year loan term. When the loan hits the adjustable-rate period, it typically adjusts annually. A low interest rate home loan can be the best option to apply for. Adjustable-rate mortgages , which have both fixed- and variable-rate components, are also usually issued as an amortized loan with steady installment payments over the life of the loan.

Home equity loans are typically charged at a fixed interest rate, although some lenders do offer adjustable options. Depending on the terms of your agreement, your interest rate on the new loan will stay the same, even if interest rates climb to higher levels. On the other hand, if interest rates are on the decline, then it would be better to have a variable rate loan.

He decided that someday he would buy his own house and make his parents proud. Orange Everyday customers who hold an ING Home Loan are automatically eligible for Orange Everyday Benefits, and are not required to meet this monthly criteria. SMSFSMSF Cash High variable interest rate on the cash component of your Self Managed Superannuation Fund. Home and Contents InsuranceING Home and Contents Insurance Save 30% on your first year's premium when you purchase a combined ING Home and Contents Insurance policy online. All Insurance Choose from a range of insurance options to protect you, your family and the things most special to you. All credit cards Clear and simple, with easy-to-use features so you can stay on top of your finances.

It can be any financial institution, whether it be a bank or an NBFC. ING reserves the right to change or withdraw the Promotion at any time. The statements, information and opinions contained in those reports are those of Core Logic only, and ING does not endorse or accept any liability for them. The ING Property Report is available to customers who provide their contact details for ING to contact them about products and services. • Rebates on the ATM withdrawal fees for the first 5 fee incurring ATM withdrawals (Domestic & International) on the account. • also make at least 5 card purchases that are settled (and not at a 'pending status') using your ING debit or credit card .

No comments:

Post a Comment